Abstract

Defined benefit pension schemes accumulate assets with the ultimate objective of honoring their obligation to the beneficiaries. Liabilities should be at the center of designing investment policies and serve as the ultimate reference point for evaluating and allocating risks and measuring performance. The goal of the investment policy should be to maximize expected excess returns over liabilities subject to an acceptable level of risk that is expressed relative to liabilities. In this article, we argue for the use of a liability-relative drawdown optimization approach to construct investment portfolios. Asset and liability returns are simulated using a vector autoregressive process with state variables. We find that drawdown optimal portfolios provide better downside protection, are better diversified and tend to be less equity centric while providing higher expected returns compared to surplus variance portfolios.

Similar content being viewed by others

Notes

Some of the uncertainty embedded in pension liabilities, such as mortality risk and wage growth uncertainty, cannot (currently) be hedged away.

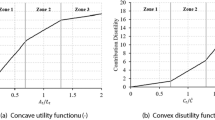

Maximizing expected utility over the funded ratio is closely related to maximizing the expected utility of the fund surplus (A T −L T ), as in Rudolf and Ziemba (2004), as the funded ratio is equal to the value of the fund surplus scaled by the value of the liabilities: F T =(A T −L T )/L T +1. An advantage of the funded ratio is that it is non-negative by definition and therefore more suited for traditional power utility functions (including logarithmic utility).

Several studies have shown that historical hedge fund returns are biased upwards because of survivorship bias and other reporting biases. Estimates of survivorship bias in hedge fund returns range from about 1.8 per cent to 2.4 per cent per annum.

For quarterly data, we find that setting λ equal to 0.18 produces the best overall fit to the yield curve data. A value of 0.18 on a quarterly basis is identical to λ=0.06 on a monthly basis, as used by Diebold and Li (2006).

Starting values for the VAR process in the simulation are the latest observed values in our sample (2008:Q3). We use antithetic sampling from the error distribution to generate the scenarios.

The original Calmar ratio is the ratio of compound annualized return to maximum drawdown.

References

Artzner, P., Delbaen, F., Eber, J. and Heath, D. (1998) Coherent measures of risk. Mathematical Finance 9: 203–228.

Barberis, N. (2000) Investing for the long run when returns are predictable. Journal of Finance 55: 225–264.

Basu, D., Oomen, R. and Stremme, A. (2006) How to Time the Commodity Market. Cass Business School. Technical report.

Bernadell, C., Coche, J. and Nyholm, K. (2005) Yield Curve Prediction for the Strategic Investor. European Central Bank, No. 472. Technical report.

Bliss, R. (1997) Testing term structure estimation methods. Advances in Futures and Options Research 9: 197–231.

Brandt, M. (2009) Portfolio choice problems. In: Y. Ait-Sahalia and L. Hansen (eds.) Handbook of Financial Econometrics. Amsterdam: North-Holland Publishers, pp. 269–336.

Campbell, J., Chan, Y. and Viceira, L. (2003) A multivariate model of strategic asset allocation. Journal of Financial Economics 67: 41–80.

Campbell, J., Lo, A. and MacKinlay, G. (1997) The Econometrics of Financial Markets. Princeton, NJ: Princeton University Press.

Campbell, J. and Viceira, L. (2002) Strategic Asset Allocation. Oxford: Oxford University Press.

Campbell, J. and Viceira, L. (2005) The term structure of the risk-return trade-off. Financial Analysts Journal 61: 34–44.

Campbell, S. and Diebold, F. (2009) Stock returns and expected business conditions: Half a century of direct evidence. Journal of Business and Economic Statistics 27: 266–278.

Carino, D. et al (1994) The Russell-Yasuda Kasai model: An asset/liability model for a Japanese insurance company using multistage stochastic programming. Interfaces 24: 29–49, Reprinted in Ziemba, W.T. and Mulvey, J.M. (eds.) (1998) World Wide Asset and Liability Modeling, Chapter 24. Cambridge University Press, pp. 609–633.

Chekhlov, A., Uryasev, S. and Zabarankin, M. (2005) Drawdown measure in portfolio optimization. International Journal of Theoretical and Applied Finance 8: 13–58.

Consigli, G. and Dempster, M. (1998) Dynamic stochastic programming for asset-liability management. Annals of Operations Research 81: 131–162.

Diebold, F. and Li, C. (2006) Forecasting the term structure of government bond yields. Journal of Econometrics 130: 337–364.

Gorton, G. and Rouwenhorst, K. (2006) Facts and fantasies about commodity futures. Financial Analyst Journal 62: 47–68.

Grossman, S. and Zhou, Z. (1993) Optimal investment strategies for controlling drawdowns. Mathematical Finance 3: 241–276.

Guidolin, M. and Timmermann, A. (2006) An econometric model of nonlinear dynamics in the joint distribution of stock and bond returns. Journal of Applied Econometrics 21: 1–22.

Guidolin, M. and Timmermann, A. (2007) Asset allocation under multivariate regime switching. Journal of Economic Dynamics and Control 31: 3503–3544.

Hoevenaars, R.P., Molenaar, R.D., Schotman, P.C. and Steenkamp, T.B. (2008) Strategic asset allocation with liabilities: Beyond stocks and bonds. Journal of Economic Dynamics and Control 32 (9): 2939–2970.

Kouwenberg, R. (2001) Scenario generation and stochastic programming models for asset liability management. European Journal of Operational Research 134: 51–64.

Kouwenberg, R., Mentink, A., Schouten, M. and Sonnenberg, R. (2009) Estimating value-at-risk of institutional portfolios with alternative asset classes. In: G. Gregoriou (ed.) The VaR Modeling Handbook: Practical Applications in Alternative Investing, Banking, Insurance, and Portfolio Management. New York: McGraw Hill, pp. 33–54.

Kouwenberg, R. and Zenios, S. (2006) Stochastic programming models for asset liability management. In: S. Zenios and W. Ziemba (eds.) Handbook of Asset and Liability Management. Amsterdam: North-Holland Publishers, pp. 253–303.

Kusy, M. and Ziemba, W. (1986) A bank asset and liability management model. Operations Research 34 (3): 356–376.

Lettau, M. and Ludvigson, S. (2001) Consumption, aggregate wealth and expected stock returns. Journal of Finance 56: 815–849.

Markowitz, H. (1952) Portfolio selection. Journal of Finance 7: 77–91.

McCulloch, J. and Kwon, H. (1993) US Term Structure Data 1947–1991. Ohio State University. Technical Report 93–6.

Mulvey, J. and Vladimirou, H. (1992) Stochastic network programming for financial planning problems. Management Science 38: 1642–1664.

Nelson, C. R. and Siegel, A. F. (1987) Parsimonious modelling of yield curves. Journal of Business 60: 473–489.

Reveiz, A. and Leon, C. (2008) Efficient Portfolio Optimization in the Wealth Creation and Maximum Drawdown Space. Banco de la Republica de Colombia. Technical report.

Rudolf, M. and Ziemba, W. (2004) Intertemporal surplus management. Journal of Economic Dynamics and Control 28: 975–990.

Sharpe, W. and Tint, L. (1990) Liabilities – A new approach. Journal of Portfolio Management 16 (Winter): 5–10.

Shiller, R. (2000) Irrational Exuberance. Princeton, NJ: Princeton University Press.

Stambaugh, R. (1997) Analyzing investments whose histories differ in length. Journal of Financial Economics 45: 285–331.

Zenios, S. (1995) Asset/liability management under uncertainty for fixed-income. Annals of Operations Research 59: 77–97.

Acknowledgements

We thank two anonymous referees for valuable comments and suggestions.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Berkelaar, A., Kouwenberg, R. A liability-relative drawdown approach to pension asset liability management. J Asset Manag 11, 194–217 (2010). https://doi.org/10.1057/jam.2010.13

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/jam.2010.13