1999-12-08

Combined forecasts from linear and nonlinear time series models

Publication

Publication

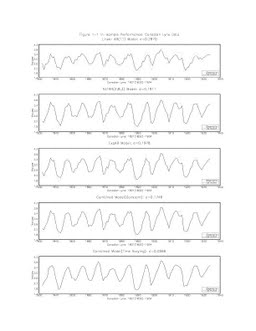

Combined forecasts from a linear and a nonlinear model are investigated for time series with possibly nonlinear characteristics. The forecasts are combined by a constant coefficient regression method as well as a time varying method. The time varying method allows for a locally (non)linear model. The methods are applied to data from two kinds of disciplines: the Canadian lynx and sunspot series from the natural sciences, and Nelson-Plosser's U.S. series from economics. It is shown that the combined forecasts perform well, especially with time varying coefficients. This result holds for out of sample performance for the sunspot and Canadian lynx number series, but it does not uniformly hold for economic time series.

| Additional Metadata | |

|---|---|

| , , , , | |

| hdl.handle.net/1765/1621 | |

| Econometric Institute Research Papers | |

| Organisation | Erasmus School of Economics |

|

Terui, N., & van Dijk, H. (1999). Combined forecasts from linear and nonlinear time series models (No. EI 9949-/A). Econometric Institute Research Papers. Retrieved from http://hdl.handle.net/1765/1621 |

|